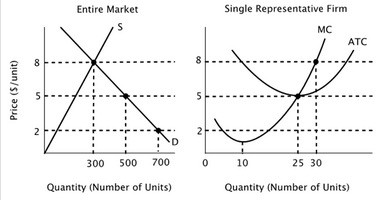

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves. In the long run equilibrium in this market:

In the long run equilibrium in this market:

A. price will equal $5, and there will be 20 firms in the industry.

B. price will equal $5, and there will be 10 firms in the industry.

C. price will equal $5 and total output will equal 500 units, but there is not enough information to determine how many firms will be in the industry.

D. price will equal $8, and there will be 20 firms in the industry.

Answer: A

You might also like to view...

The figure above shows the market for transportation services, which produces an external cost due to the air pollution that is created. Suppose that the government decides to introduce a pollution tax

What is the tax per vehicle mile that will achieve the efficient outcome? A) $2 B) $4 C) $6 D) $8

How did McDonalds address the drive-through innovation in China?

What will be an ideal response?

National income is calculated by subtracting ____ from GDP

a. depreciation. b. investment and net exports. c. Social Security insurance contributions and transfer payments. d. corporate and personal income taxes.

The MR = MC rule is no longer accepted by most economists as representing the behavior of firms

Indicate whether the statement is true or false