Define marginal cost. Is it different from the concept of willingness to accept?

What will be an ideal response?

Marginal cost in production refers to the extra cost incurred in producing an additional unit of a commodity. Willingness to accept is the lowest price that a firm is willing to receive to sell an additional unit. In a competitive market, marginal cost is the same as a seller's willingness to accept. This is because the lowest price that any seller is willing to accept for an additional unit will equal the marginal cost of production of that unit. If he asks for a higher price, he will lose almost all of his buyers, and if he asks for a lower price, his cost of producing an additional unit will exceed the revenue he makes from selling it.

You might also like to view...

If the reserve ratio is 10 percent, the money multiplier is equal to 10

Indicate whether the statement is true or false

If the cross elasticity of demand between goods A and B is positive

A) the demands for A and B are both price elastic. B) the demands for A and B are both price inelastic. C) A and B are complements. D) A and B are substitutes.

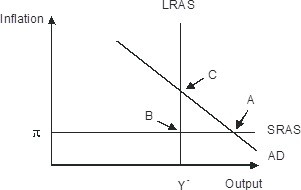

Refer to the figure below. In response to gradually falling inflation, this economy will eventually move from its short-run equilibrium to its long-run equilibrium. Graphically, this would be seen as

A. long-run aggregate supply shifting leftward B. Short-run aggregate supply shifting upward C. Short-run aggregate supply shifting downward D. Aggregate demand shifting leftward

If the first copy cost of a music video is $223,000 and the marginal cost is $0, then as the firm produces an infinite quantity of the video, the average total cost of producing the video will approach:

A. zero. B. $1.00. C. $2,230. D. $1 million.