When the price faced by a competitive firm was $5, the firm produced nothing in the short run. However, when the price rose to $10, the firm produced 100 tons of output. From this we can infer that

A) the firm's marginal cost curve must be flat.

B) the firm's marginal costs of production never fall below $5.

C) the firm's average cost of production was less than $10.

D) the firm's total cost of producing 100 tons is less than $1000.

E) the minimum value of the firm's average variable cost lies between $5 and $10.

E

You might also like to view...

"The short-run Phillips curve is vertical at the natural unemployment rate." Is the previous statement correct or incorrect?

What will be an ideal response?

A free market fails when

A) firms that produce goods which create positive externalities go bankrupt. B) firms that produce goods which create negative externalities earn high profits. C) there is an external effect in either production, consumption, or both. D) there is government intervention.

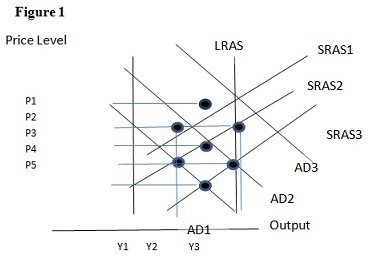

Using Figure 1 above, if the aggregate demand curve shifts from AD2 to AD3 the result in the short run would be:

A. P1 and Y2. B. P2 and Y3. C. P3 and Y1. D. P2 and Y2.

Starting from potential output, if consumer confidence decreases and consumers decide to spend less, then this will generate a(n) ________ gap and inflation will ________.

A. expansionary; decrease B. recessionary; decrease C. recessionary; increase D. expansionary; increase