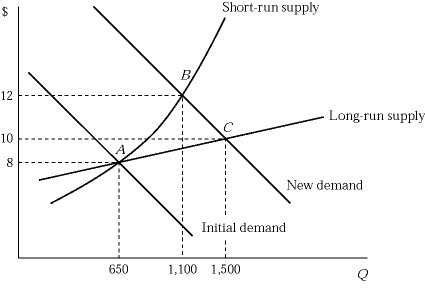

Figure 9.5Figure 9.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, what will happen to the number of firms in the industry as the industry moves from point A to point B?

Figure 9.5Figure 9.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, what will happen to the number of firms in the industry as the industry moves from point A to point B?

A. It increases.

B. It decreases.

C. It remains the same.

D. either It increases or It decreases or It remains the same

Answer: C

You might also like to view...

A monopolistically competitive firm can convince buyers that its product has value by differentiating its product to suit consumers' preferences

Indicate whether the statement is true or false

Endogenous growth models

a. predict absolute convergence. b. predict conditional convergence. c. do not predict convergence. d. predict convergence among rich countries but not poor countries.

Which of the following statements about marginal cost is correct?

a. If the cost to produce one more unit of output is lower than the previous average cost, then producing one more unit brings down the average. b. Marginal cost is a calculation of the cost of one unit of output, and therefore it can have no effect on average costs. c. As the cost per change in one unit of output increases, average costs of production decrease in an inverse relationship. d. The cost of producing one more unit of output decreases as output grows, whereas average costs rise with output.

Jobs lost to outsourcing can be partially offset by jobs gained from:

A. higher production costs. B. higher opportunity costs. C. greater trade imbalances. D. increased output from another industry.