What is productivity?

What will be an ideal response?

The amount of output from a unit of an input

You might also like to view...

A shortage exists in a market if

a. there is an excess supply of the good. b. quantity supplied exceeds quantity demanded. c. the current price is below its equilibrium price. d. All of the above are correct.

A. a firm may realize excessively large profits. B. workers may provide less-than-expected work effort. C. compensating wage differences do not pay for differences in the nonmonetary aspects of jobs. D. human capital investments vary among

workers. A. principals and agents share a common interest, leading to free-rider problems. B. principals and agents are in an adversarial role, sharing no common interests. C. principals pursue some of their own objectives, which may conflict with the objectives of the agents. D. agents pursue some of their own objectives, which may conflict with the objectives of the principals.

Explain why nominal wages are a function of the expected price level

What will be an ideal response?

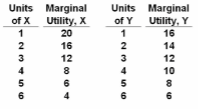

Refer to the data. Which of the following represents the demand schedule for X?

Answer the question on the basis of the following marginal utility data for products X and Y. Assume that the prices of X and Y are $4 and $2 respectively and that the consumer's income is $18.