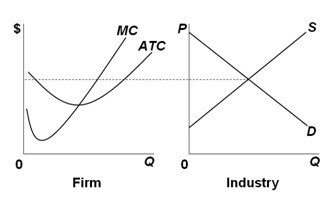

Use the following graphs for a perfectly competitive market in the short run to answer the next question. The graphs suggest that in the long run, assuming no changes in the given information,

The graphs suggest that in the long run, assuming no changes in the given information,

A. buyers will leave the industry.

B. more buyers will come to the market.

C. some firms will exit from this industry.

D. new firms will enter the industry.

Answer: D

You might also like to view...

In an economy in which the skills, preferences, and motivations of workers vary widely, equality of wage rates would

a. lead to shortages and surpluses of resources and the use of involuntary methods of achieving work participation. b. result in a variety of product prices, but overall GDP would be unaffected. c. be efficient if the wages were fixed at a high enough level. d. reduce the productive incentives of high-skill workers, an effect that would be offset by the increased work effort of low-skill workers.

Below are pairs of GDP growth rates and unemployment rates. Economists would not be shocked to see most of these pairs in the U.S. Which pair of GDP growth rates and unemployment rates is not realistic?

a) 10 percent; 5 percent b) -1 percent; 8 percent c) 3 percent; 6 percent d) -2 percent; 2 percent

When the free rider problem is present in a market:

A. the good is rival in consumption. B. the good will likely be overconsumed. C. what people pay often does not reflect the real value they put on a good. D. the good is easily excludable.

The difference between average total costs and average variable costs is:

A. marginal cost. B. fixed cost. C. average fixed cost. D. None of the statements is correct.