In economic utility analysis, consumer tastes and preferences are assumed

A. given but rapidly changeable.

B. given and stable for an individual.

C. to be determined by income.

D. to be influenced by the prices of goods.

Answer: B

You might also like to view...

A trade surplus occurs when a country's exports exceed that country's imports

Indicate whether the statement is true or false

Refer to Figure 28-1. Suppose that the economy is currently at point A, and the unemployment rate at A is the natural rate. What policy would the Federal Reserve pursue if it wanted the economy to move to point C in the long run?

A) Sell treasury bills. B) Increase the money supply. C) Lower the discount rate. D) Buy treasury bills. E) No policy will move the economy to point C in the long run.

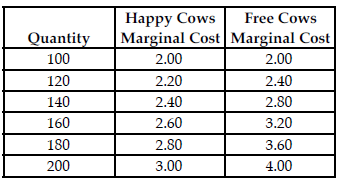

Refer to the table below. Suppose the perfectly competitive market for dairy products had a 40 percent chance of a high price of $3.00 and a 60 percent chance of a low price of $2.00. However, both Happy Cows and Free Cows have revised their probabilities and now believe that the probability of a high price of $3.00 is 80 percent and the probability of a low price of $2.00 is 20 percent. If the

managers of Happy Cows want to maximize expected profit based on the new probabilities by how much will they change the quantity produced?

Happy Cows and Free Cows are two separate perfectly competitive dairy farms. The table above shows the respective firms' marginal cost at various production levels.

A) Happy Cows will decrease their production by 20 units.

B) Happy Cows will decrease their production by 40 units.

C) Happy Cows will increase their production by 40 units.

D) Happy Cows will increase their production by 20 units.

Refer to the above table. If the price of the good produced is $8, the marginal revenue product of the 12th worker is

A) $720 B) $800 C) $5520 D) $560