Gross domestic product (GDP) is

A) the value of all final goods and services produced in a country during a year.

B) the sum of consumption expenditure, investment, government expenditure on goods and services, and net exports.

C) the sum of compensation of employees, proprietors' income, net interest, rental income, corporate profits, depreciation, and indirect business taxes minus subsidies.

D) all of the above.

D

You might also like to view...

For a typical firm, the portion of the AC curve that is downward-sloping is because production

A. exhibits decreasing returns to scale. B. creates innovative technological progress. C. economies of scale. D. exhibits rising total product.

The cost that does not change as output changes is

A) total fixed cost. B) average fixed cost. C) total variable cost. D) average variable cost. E) marginal cost.

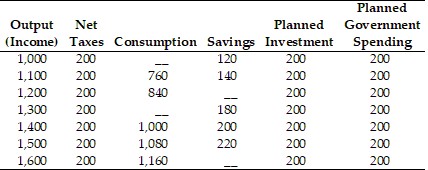

Refer to the information provided in Table 24.5 below to answer the question(s) that follow.Table 24.5All Numbers are in $ Million Refer to Table 24.5. Assuming constant MPC, at income of $1,200 million, saving is $________ million, at income of $1,600 million, saving is $________ million.

Refer to Table 24.5. Assuming constant MPC, at income of $1,200 million, saving is $________ million, at income of $1,600 million, saving is $________ million.

A. 160; 240 B. 170; 250 C. 150; 230 D. 180; 260

Refer to the data provided in Table 17.2 below to answer the following question(s). The table shows the relationship between income and utility for Sue.Table 17.2 IncomeTotal Utility $00$20,00020$40,00040$60,00060$80,00080Refer to Table 17.2. Sue earns $40,000 annually. She has the opportunity to bet her entire salary on the upcoming super bowl. If Sue takes the bet, she will pick the Patriots. She believes that the Patriots have a 50-50 chance of winning the game. If the Patriots win, Sue will win $81,000 but if they lose she loses her entire salary ($0). Will Sue take the bet?

A. yes B. no C. maybe D. indeterminate from the given information