If the price of rubber (an input to the production of tires) increases:

A. the supply of tires will decrease.

B. the demand for tires will decrease

C. the demand for tires will increase.

D. the supply of tires will increase.

Answer: A

You might also like to view...

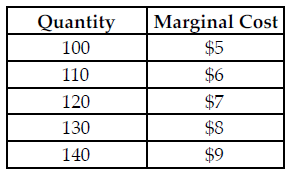

Refer to the table below. The perfectly competitive firm has a random demand with a 50 percent chance of being $7 and a 50 percent chance of being $9. What quantity should the firm produce to maximize its expected profit?

The above table summarizes the marginal cost of production at various quantity levels for a perfectly competitive firm.

A) 130

B) 110

C) 120

D) 140

The distinguishing of products by brand name, color, and other attributes

A) is known as interdependence. B) is known as product differentiation. C) leads to many firms in the market. D) leads to collusion.

The value of a good

a. depends on many factors, including who uses it and under what circumstances. b. is determined by the cost of producing it. c. depends on the labor necessary to supply the good. d. can be measured objectively by a survey of manufacturers of the good.

Refer to the information provided in Table 14.5 below to answer the question that follows. Table 14.5B's Strategy ?AdvertiseDon't Advertise??A's profit $200 millionA's profit $400 million?AdvertiseB's profit $200 millionB's profit $100 millionA's Strategy????Don'tA's profit $100 millionA's profit $150 million?AdvertiseB's profit $400 millionB's profit $150 millionRefer to Table 14.5. What is the Nash equilibrium in the game?

A. (Advertise, Advertise) B. (Advertise, Don't Advertise) C. (Don't Advertise, Don't Advertise) D. (Don't Advertise, Advertise)