When firms are neither entering nor exiting a perfectly competitive market,

a. total revenue must equal total cost for each firm.

b. economic profits must be zero.

c. price must equal the minimum of marginal cost for each firm.

d. Both a and b are correct.

d

You might also like to view...

"It is clear from the theory of monopolistic competition that product development is not pushed to its efficient level." This statement is

A) false because there is so much product differentiation in monopolistic competition. B) true because there is little incentive to innovate in monopolistic competition. C) false because there are so many wasteful innovations in monopolistic competition that are merely cosmetic. D) true because price exceeds marginal revenue in monopolistic competition.

An item has utility for a consumer if it

A) generates enjoyment or satisfaction. B) is scarce. C) is something everyone else wants. D) has a high price.

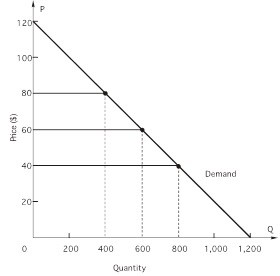

In the figure above, what is the interval elasticity of demand over the price range $60 to $80?

In the figure above, what is the interval elasticity of demand over the price range $60 to $80?

A. -0.75 B. -2.00 C. -1.40 D. -1.00 E. -1.10

Shifts in factor demand result from changes in

A. demand for outputs. B. the price of other inputs. C. the quantity of other factors with which it works. D. All of the above are correct.