Use an isocost-isoquant diagram to explain how a firm determines the least cost combination of labor and capital to produce a given level of output. What is true of the marginal product per dollar at the least cost combination of capital and labor? Why?

What will be an ideal response?

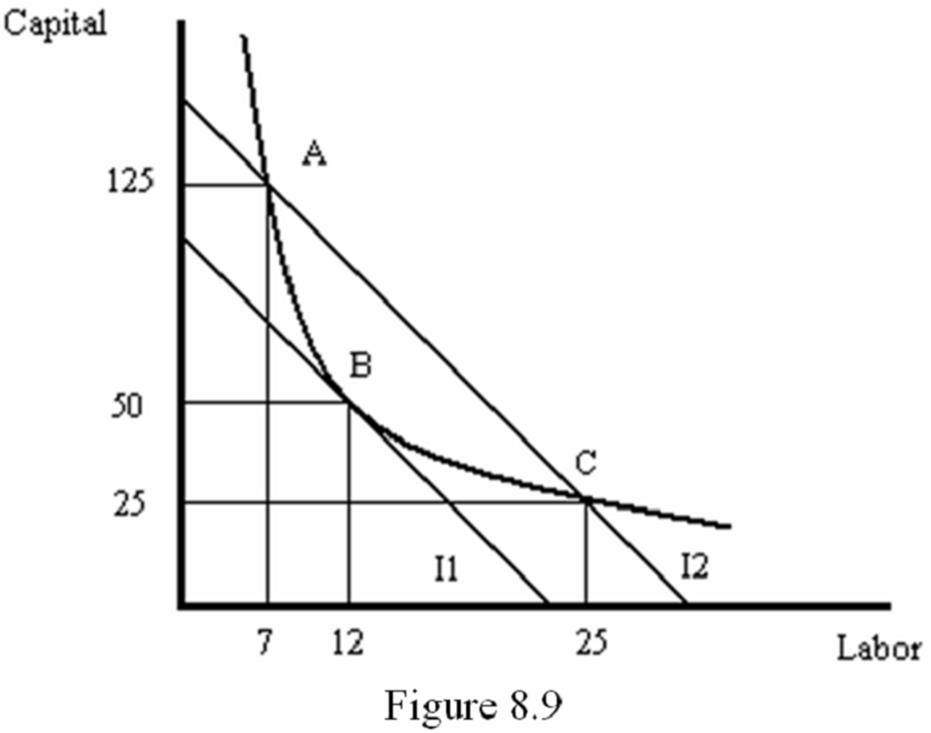

Refer to Figure 8.9, which shows an isoquant and two isocost lines. The least-cost combination of capital and labor is on the lowest isocost line that is just tangent to the isoquant that represents the given level of output.

In Figure 8.9, the level of output represented by the isoquant can be produced with three different combinations of capital and labor, represented by the points labeled A, B and C. Since combinations A and C are on a higher isocost line, they would cost more than the combination represented by point B. In fact, point B is on the lowest isocost line. Since the isocost line and isoquant are tangent at point B, their slopes are equal at that point. The slope of the isocost line is - (wage rate/rental rate of capital L) and the slope of the isoquant is equal to MPL/MPK. Thus, at point B:

MPL/MPK = wage rate/rental rate of capital

MPL/wage rate = MPK/rental rate of capital

This last equation implies that, at the least-cost combination of capital and labor, the marginal product per dollar spent on labor must equal the marginal product per dollar spent on capital.

You might also like to view...

The value of the U.S. dollar bill is determined by

A) the quantity of gold in Fort Knox. B) the quantity of gold in the Federal Reserve. C) the quantity of gold in circulation. D) the gold futures market. E) none of the above.

In the short run, a supply shock that shifts the short-run aggregate supply curve leftward raises the price level and increases real GDP

Indicate whether the statement is true or false

Which of the following workers is most likely to be asked to post a performance bond?

A) construction contractor B) fast food worker C) economics professor D) book author

Average total cost equals

a. change in total costs divided by quantity produced. b. change in total costs divided by change in quantity produced. c. (fixed costs + variable costs) divided by quantity produced. d. (fixed costs + variable costs) divided by change in quantity produced.