In a perfectly competitive market, when the price is greater than the minimum average total cost for most firms, some will:

A. exit until the price increases to equal minimum ATC.

B. enter until the price increases to equal minimum ATC.

C. exit until the price drops to equal minimum ATC.

D. enter until the price drops to equal minimum ATC.

Answer: D

You might also like to view...

Which of the following increases aggregate supply in the short-run, everything else held constant?

A) an increase in the price of crude oil B) a successful wage push by workers C) expectations of a higher inflation D) a technological improvement that increases worker productivity

If losses are incurred in a competitive industry, then over the long-run we can expect a greater quantity supplied, because market price will rise

a. True b. False Indicate whether the statement is true or false

Which of the following could explain a decrease in labor supply to a particular labor market?

a. an increased preference for this type of work b. a decrease in the size of the population c. an increase in the number of firms in the market d. a leftward shift of the marginal revenue product curve of labor at a typical firm e. a reduction in wages rates for similar types of work

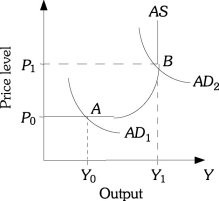

Refer to the information provided in Figure 29.2 below to answer the question(s) that follow. Figure 29.2Refer to Figure 29.2. If the economy is currently at Point B and policy makers implement a policy which shifts the aggregate demand curve to AD1, the time the economy needs to make the adjustment is known as the

Figure 29.2Refer to Figure 29.2. If the economy is currently at Point B and policy makers implement a policy which shifts the aggregate demand curve to AD1, the time the economy needs to make the adjustment is known as the

A. implementation lag. B. recognition lag. C. frictional lag. D. response lag.