The opportunity cost of an economic decision is:

a. the best alternative that was sacrificed.

b. the amount of money needed to implement the decision.

c. any land, labor, and capital that are wasted.

d. all options that were lost due to scarcity.

a

You might also like to view...

Banks will keep excess reserves when

A. they do not foresee profitable opportunities to make loans. B. business conditions generally are depressed. C. they do not foresee opportunities to make secure loans. D. All of these responses are correct.

Under the theory of perfect competition, firms and buyers know the availability and prices associated with all products in the market

a. True b. False Indicate whether the statement is true or false

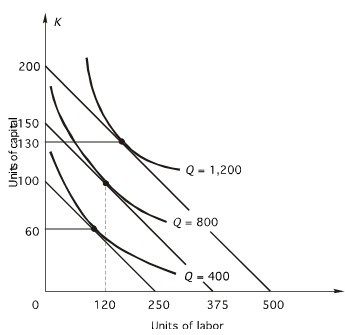

Refer to the following figure. The price of capital is $50 per unit: The minimum cost of producing 800 units of output is

The minimum cost of producing 800 units of output is

A. $10,000. B. $8,000. C. $7,500. D. $6,000.

Suppose the market for bottled water is served by two oligopolists. If they reach an agreement to restrict production and charge a price above marginal cost, then:

A. neither firm will have an incentive to cheat on the agreement since it benefits them both. B. they will earn a larger profit than a monopolist would have earned. C. their agreement is likely to eventually collapse. D. they will charge a higher price than a monopolist would have charged.