If firms in a perfectly competitive industry are earning positive economic profits, then what will happen in the long run?

What will be an ideal response?

Economic profits provide incentives for entrepreneurs to start new firms and enter the industry. When entry of new firms takes place, the market supply curve shifts outward. The equilibrium quantity increases, and the market clearing price declines. This pushes economic profits back down toward zero. When economic profits return to zero, there is no longer an incentive for new firms to enter the industry, and a new long-run equilibrium will have been reached.

You might also like to view...

Define logrolling. Explain why logrolling often results in legislation that benefits the economic interests of a few, while harming the interests of a larger group of people

What will be an ideal response?

The model yt = et+  1et -1 + 2et -2 , t = 1, 2, ….. , where etis an i.i.d. sequence with zero mean and variance

1et -1 + 2et -2 , t = 1, 2, ….. , where etis an i.i.d. sequence with zero mean and variance

data-wiris-created="true" src="@@PLUGINFILE@@/ppg__cognero__Ch_11_Further_Issues_in_Using_OLS_with_Time_Sries_Data__media__bb4e0354-3643-43f7-80ca-ddc661bf830b.PNG" style="vertical-align:middle;" />2e represents a(n): A. static model. B. moving average process of order one. C. moving average process of order two. D. autoregressive process of order two.

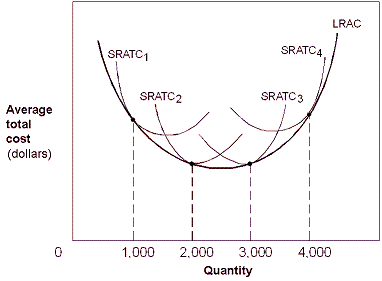

Exhibit 6-14 Cost curves

?

In Exhibit 6-14, economies of scale only exist for output levels up to:

In Exhibit 6-14, economies of scale only exist for output levels up to:

A. 1,000. B. 2,000. C. 3,000. D. 4,000.

Jose has one evening in which to prepare for two exams and can employ one of two possible strategies: The opportunity cost of receiving a 93 on the economics exam is __________ points on the statistics exam.

ANSWER 4.png)