When average total cost is decreasing as output expands:

a. average fixed cost must be increasing

b. average variable cost must be falling.

c. marginal cost must be greater than average total cost.

d. marginal cost must be less than average total cost.

d

You might also like to view...

Under which type of market structure is the firm’s pricing decision the most difficult?

a. perfect competition b. monopoly c. monopolistic competition d. oligopoly

The short-run Phillips curve is downward sloping but the long-run is a vertical line

a. True b. False Indicate whether the statement is true or false

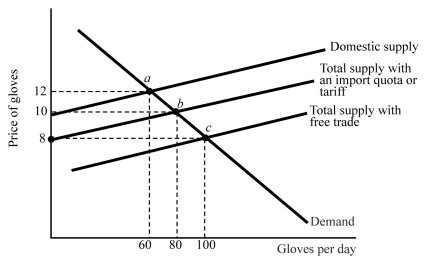

Refer to Figure 18.1. With free trade, what is the equilibrium quantity of gloves in Duckland?

Refer to Figure 18.1. With free trade, what is the equilibrium quantity of gloves in Duckland?

A. 100 B. 80 C. 60 D. 40

The value of the four-firm concentration ratio that many economists consider indicative of the existence of an oligopoly in a particular industry is

A) anything greater than 10 percent. B) anything greater than 20 percent. C) anything greater than 30 percent. D) anything greater than 40 percent.