The short-run supply curve of a perfectly competitive industry with firms having identical costs is:

a. a horizontal line at the market price.

b. a vertical line at the equilibrium output.

c. an upward rising curve.

d. a downward sloping step function.

C

You might also like to view...

The use of signals in a market economy

a. makes everyone better off, even those people who choose not to obtain the signal. b. prevents the economy from reaching an equilibrium. c. lowers efficiency because the signals waste resources. d. is one way that the principal-agent problem can be avoided.

When there are very few substitutes for a good, the demand for the good will tend to be

A) inelastic. B) elastic. C) unitary. D) perfectly elastic.

Assume that crackers and soup are complementary goods. The effect on the soup market of an increase in the price of crackers (other things being equal) would best be described as a(n):

a. decrease in the quantity of soup demanded. b. decrease in the demand for soup. c. increase in the quantity of soup demanded. d. increase in the demand for soup.

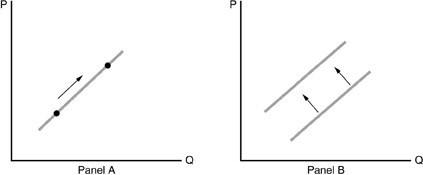

Refer to the above figure. Which of the following statements is TRUE?

Refer to the above figure. Which of the following statements is TRUE?

A. Panel A shows a change in quantity supplied and Panel B shows a change in supply. B. Panel A shows a change in supply and Panel B shows a change in quantity supplied. C. Panel A shows an increase in supply and Panel B shows a decrease in supply. D. Both Panels A and B show an increase in supply.