Fluctuations in employment and output result from changes in

a. aggregate demand only.

b. aggregate supply only.

c. aggregate demand and aggregate supply.

d. neither aggregate demand nor aggregate supply.

c

You might also like to view...

Consider the market for credit. When the demand for credit decreases while the supply of credit remains unchanged,

A) the interest rate will decrease and the amount of credit provided in the market will increase. B) the interest rate will increase and the amount of credit provided in the market will increase. C) the interest rate will decrease and the amount of credit provided in the market will decrease. D) the interest rate will increase and the amount of credit provided in the market will decrease.

If the inputs to a production process are perfect complements, the firm can choose from a virtually infinite array of combinations of the two inputs to minimize the costs of producing a given level of output

Indicate whether the statement is true or false

A famous cartel that dramatically increased the price of oil in the mid-1970s was

a. OTEC b. IMF c. OECD d. OPEC e. LDC

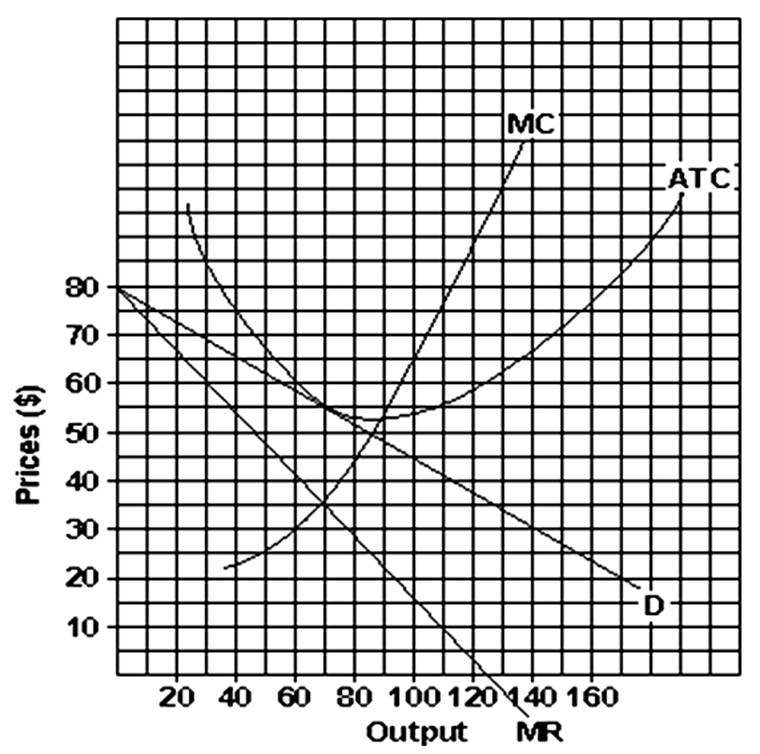

You could conclude that

A. new firms will enter the industry.

B. existing firms will leave the industry.

C. the industry is in the long run.