At a perfectly competitive firm's short-run equilibrium level of output,

a. P = MR = MC.

b. P = MR, but MR does not equal MC.

c. P = MC, but MR does not equal MC.

d. MR = MC and P < MR.

a

You might also like to view...

If a firm's short-run average cost curves are u-shaped, does this imply that the long-run average cost curve must also be u-shaped?

What will be an ideal response?

In a perfectly competitive market, the

a. market demand curve is horizontal b. short-run market supply curve is horizontal c. short-run market demand curve slopes upward d. short-run market supply curve slopes downward e. market demand curve slopes downward

FGLS estimates are efficient when explanatory variables are not strictly exogenous.

Answer the following statement true (T) or false (F)

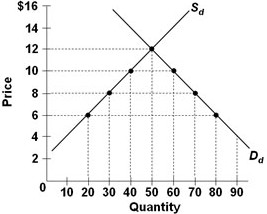

Use the following graph, where Sd and Dd are the domestic supply and demand curves for a product, to answer the next question. The world price of the product is $6. If the market is open to international trade but there is a tariff of $2 per unit imposed, the total government revenue generated by the tariff would be

The world price of the product is $6. If the market is open to international trade but there is a tariff of $2 per unit imposed, the total government revenue generated by the tariff would be

A. $100. B. $60. C. $80. D. $40.