Efficiency in a market is achieved when

a. a social planner intervenes and sets the quantity of output after evaluating buyers' willingness to pay and sellers' costs.

b. the sum of producer surplus and consumer surplus is maximized.

c. all firms are producing the good at the same low cost per unit.

d. no buyer is willing to pay more than the equilibrium price for any unit of the good.

b

You might also like to view...

It is ________ profit maximizing for firms to dump in foreign markets

A) never B) sometimes C) always

The key goal of monetary policy is to..

What will be an ideal response?

Which one of the following is the best example of an oligopolistic industry?

A. long-distance telephone service B. wheat growers C. apple growers D. public utilities

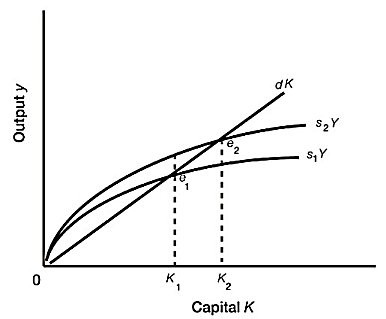

Refer to Figure 13A.2. If the economy were saving at the rate s1:

Refer to Figure 13A.2. If the economy were saving at the rate s1:

A. saving would equal depreciation at e1. B. capital stock would increase until the economy reached K2. C. the economy would grow until it reached e2. D. All of these.