Accounting profit differs from economic profit because:

a. of differences in the manner in which revenue is calculated.

b. economic costs include depreciation, while accounting costs do not.

c. accounting costs are generally higher than economic costs because accounting costs include explicit and implicit costs, while economic costs include only explicit costs.

d. economic costs are generally higher than accounting costs because economic costs include all opportunity costs, while accounting costs include explicit costs only.

Answer: d. economic costs are generally higher than accounting costs because economic costs include all opportunity costs, while accounting costs include explicit costs only.

You might also like to view...

Refer to Table 16-3. Suppose Julie's marginal cost of providing this service is constant at $7 and she charges $7. How many hours will be purchased and what is her total revenue?

A) 5 hours; total revenue = $35 B) 4 hours; total revenue = $28 C) 3 hours; total revenue = $21 D) 2 hours; total revenue = $14

A firm that sells at a price below average cost is losing money

a. True b. False Indicate whether the statement is true or false

Which of the following is most consistent with economizing behavior?

a. If you derive the same satisfaction from eating pizza and eating ice cream, it makes no difference which one of the two you choose. b. Before voting, you should invest the time and energy to become fully informed on all of the issues and candidates. c. It never makes sense to hire someone to do something for you that you could do yourself. d. If you get the same satisfaction from a chicken sandwich and a salad, you should purchase the one that costs the least.

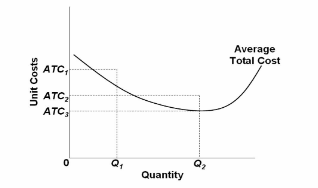

Refer to the long-run cost diagram for a firm. If the firm produces output Q 2 at an average cost of ATC 3 , then the firm is:

A. producing the profit-maximizing output but is failing to minimize production costs.

B. incurring X-inefficiency but is realizing all existing economies of scale.

C. incurring X-inefficiency and is failing to realize all existing economies of scale.

D. producing that output with the most efficient combination of inputs and is realizing all existing economies of scale.