In the long run, each perfectly competitive firm produces at the lowest point on

a. its short-run average total cost curve

b. its long-run average total cost curve

c. its marginal cost curve

d. both its short-run and long-run average total cost curves

e. both its short-run average cost curve and its marginal cost curve

D

You might also like to view...

According to classical economists, the increase in unemployment in recessions is caused by

A) slack aggregate demand. B) the failure of wages to adjust to restore equilibrium in the labor market. C) the power of labor unions, which prevent firms from cutting wages. D) a mismatch of workers and jobs.

A market that has no barriers to entry and many small firms selling products that are slightly different from one another is best described as:

A. monopolistic competition. B. monopoly. C. perfect competition. D. oligopoly.

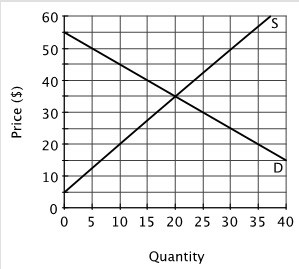

Refer to the accompanying figure. If the current market price were $20:

A. there would be an excess supply of 25 units. B. the market would be in equilibrium. C. there would be an excess demand of 25 units. D. there would be an excess demand of 35 units.

Discouraged workers

A. have jobs, but are unhappy with them. B. are officially unemployed. C. want to work, but have given up looking for jobs. D. are not working and don't want to work.