If price rises, what happens to quantity supplied of a product?

What will be an ideal response?

It increases.

You might also like to view...

Absolute advantage is the ability to produce a good using fewer inputs than another producer.

Answer the following statement true (T) or false (F)

Refer to the above figure. Which of the following statements is true about the demand curves for an individual firm in a perfectly competitive industry and a monopoly?

A) Panel A is the demand curve for a perfectly competitive firm and panel B is the demand curve for a monopoly. B) Panel C is the demand curve for a perfectly competitive firm and panel A is the demand curve for a monopoly. C) Panel C is the demand curve for a perfectly competitive firm and panel B is the demand curve for a monopoly. D) Panel B is the demand curve for a perfectly competitive firm and panel A is the demand curve for a monopoly.

We need to study a model in which real and nominal variables interact in order to understand how the economy works

a) in the short run but not the long run. b) without regards to any time period, whether the short run or the long run. c) in both the short run and the long run. d) in the long run but not the short run.

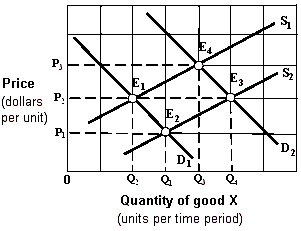

Exhibit 4-2 Supply and demand curves In Exhibit 4-2, which of the following might cause a shift from S1 to S2?

In Exhibit 4-2, which of the following might cause a shift from S1 to S2?

A. A decrease in input prices. B. A decrease in consumer prices. C. An increase in input prices. D. An increase in consumer income.