A barrier to entry in an oligopolistic industry is ______.

a. perfect competition

b. the large number of firms involved

c. the low average costs for a new entrant

d. control over important inputs

d. control over important inputs

You might also like to view...

The theory of investment that emphasizes the role of expected growth in real GDP on investment spending is known as

A) the theory of animal spirits. B) the accelerator theory. C) real business cycle theory. D) the multiplier theory.

The benefits principle is often used to justify

a. the progressive income tax. b. a flat income tax. c. a regressive excise tax. d. earmarking the proceeds from taxes for specific public services.

The law of diminishing returns results in:

A. an eventually falling marginal cost curve. B. a total product curve that eventually increases at a decreasing rate. C. an eventually rising marginal product curve. D. a total product curve that rises indefinitely.

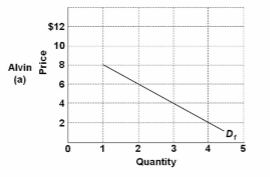

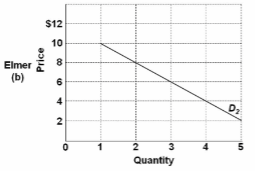

Refer to the diagrams in which figures (a) and (b) show demand curves reflecting the prices Alvin and Elmer are willing to pay for a public good, rather than do without it. If the marginal cost of the optimal quantity of this public good is $10, the

optimal quantity must be:

A. 1 unit.

B. 2 units.

C. 3 units.

D. 4 units.