When economists say that people choose rationally, this means

a. they gather all relevant information before making their purchases

b. once a pattern of behavior has been established, people tend to become set in their ways

c. people respond in predictable ways to changes in costs and benefits

d. people rarely make errors when they are permitted to make transactions

e. once made, decisions are never reversed

C

You might also like to view...

For the U.S. economy, on an average:

A) growth resulting from technology is greater than the growth resulting from human capital. B) growth resulting from technology is smaller than the growth resulting from physical capital. C) growth resulting from technology equal to the growth resulting from physical capital. D) growth resulting from technology equal to the growth resulting from human capital.

According to the real business cycle theory, an increase in an input price, such as oil, will

A) increase both real Gross Domestic Product (GDP) and the price level. B) increase real Gross Domestic Product (GDP) but not change the price level. C) decrease real Gross Domestic Product (GDP) but increase the price level. D) decrease both real Gross Domestic Product (GDP) and the price level.

For which of the following medical goods or services is the income elasticity of demand largest?

a. Emergency services after a car accident. b. Measles shots. c. Physical examinations for life insurance applications. d. Medical tests to diagnose specific symptoms. e. Face-lifts.

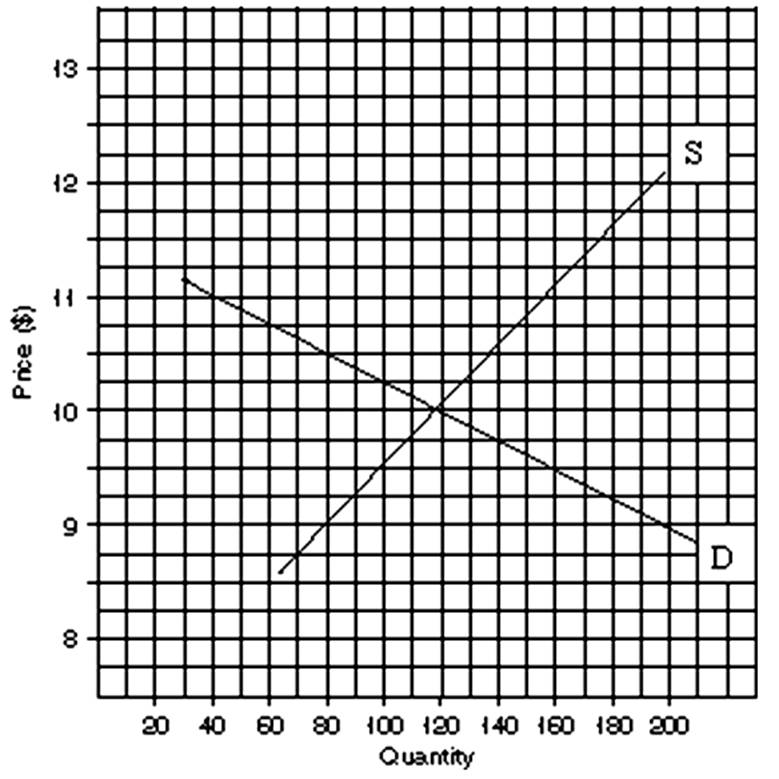

Draw another supply curve S to indicate a $1 tax increase. (a) How much of this tax is borne by the buyer? (b) How much of this tax is borne by the seller?