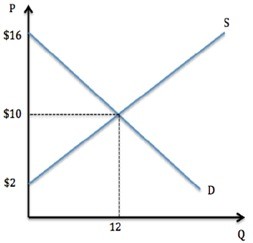

Assume the market was in equilibrium in the graph shown. If the market price gets set to $14, which of the following is true?

Assume the market was in equilibrium in the graph shown. If the market price gets set to $14, which of the following is true?

A. Some producers gain surplus, but total surplus falls.

B. Some consumers gain surplus, but total surplus falls.

C. Some consumers lose surplus, but total surplus rises.

D. Some producers lose surplus, but total surplus rises.

Answer: A

You might also like to view...

Two nations can produce computers and software in the amounts given in the table above

Does either nation have an absolute advantage in producing the products? Which nation has a comparative advantage in computers? Which nation has a comparative advantage in software? Explain your answers.

According to the menu cost theory, firms will be slow in changing their prices because

A) if prices changed frequently, individuals would reduce their demand for that good because of uncertainty. B) frequent price changes would be a sign of monopolistic behavior. C) the cost of changing the price might exceed the additional revenue the price change would generate. D) demand for their product would fall because consumers would purchase goods from firms that had not raised their prices.

Which of the following provides a measure of the overall fit of a regression?

A. The F-statistic and R-square B. F-statistic C. R-square D. t-statistic

A Japanese recession will be counteracted by an appreciation of the Japanese yen.

Answer the following statement true (T) or false (F)