Marginal cost is equal to

A. The change in total costs divided by the change in quantity produced.

B. The change in fixed costs as more units are produced.

C. Average total cost multiplied by quantity produced.

D. Total cost divided by quantity produced.

Answer: A

You might also like to view...

How do Canada and the United Kingdom deliver healthcare and what is the problem left unresolved?

What will be an ideal response?

National income is the sum of:

a. personal income and personal tax payments. b. proprietors' income, rental income, compensation of employees, corporate profits, and interest receipts, net of indirect business taxes and the capital consumption allowance. c. wages, transfer payments, interest paid to businesses, and tax revenue. d. NNP and the capital consumption allowance. e. consumption, investment, government spending, and net exports.

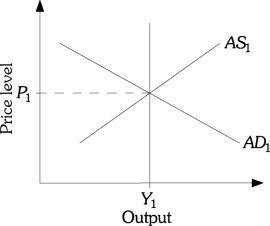

Refer to the information provided in Figure 32.2 below to answer the question(s) that follow. Figure 32.2Refer to Figure 32.2. According to monetarists, an expansionary fiscal policy in the long run and after all the adjustments have been made

Figure 32.2Refer to Figure 32.2. According to monetarists, an expansionary fiscal policy in the long run and after all the adjustments have been made

A. increases the price level above P1, but does not change equilibrium output. B. increases equilibrium output above Y1 and decreases the price level below P1. C. does not increase equilibrium output or the price level. D. increases equilibrium output above Y1, but does not change the price level.

Since 1985 which of these countries has had the fastest rate of economic growth?

A. The United States B. China C. Britain D. The former Soviet Union