To obtain the market price of a good from its factor cost one must:

(a) Add indirect taxes and subtract subsidies.

(b) Subtract indirect taxes and add subsidies.

(c) Subtract both indirect taxes and subsidies.

(d) Correctly cost all of the inputs used minus subsidies.

Answer: (a) Add indirect taxes and subtract subsidies.

You might also like to view...

Which of the following Fed actions increases the excess reserves of commercial banks?

A. Selling bonds to the public B. Selling bonds to commercial banks C. Lower the reserve requirement D. Increasing the discount rate

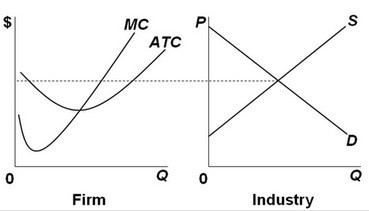

A purely competitive firm, as shown above, will face what kind of change in economic profits over the long run, assuming industry demand is constant?

A purely competitive firm, as shown above, will face what kind of change in economic profits over the long run, assuming industry demand is constant?

A. Economic profits will increase. B. Economic profits will be unchanged. C. Economic profits will decrease. D. Cannot be decided from the information given.

Which would most likely shift the aggregate supply curve? A change in:

a. Government spending b. Excess capacity in business c. Consumer expectations d. Prices of imported resources

If economists say that a 7 percent growth in the money supply will increase aggregate demand by 7 percent, they are assuming that velocity

A. will decrease. B. is constant. C. will increase. D. is unpredictable.