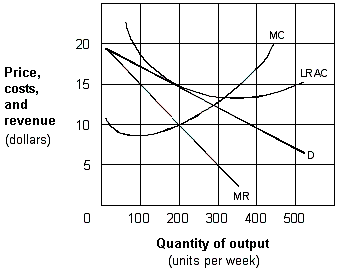

Exhibit 10-2 A monopolistic competitive firm

Comparing the firms in a monopolistic competitive industry shown in Exhibit 10-2 to a perfectly competitive firm in long-run equilibrium, we find that both firms

A. choose a price equal to the marginal cost at the profit-maximizing quantity.

B. will experience entry of new firms into the industry.

C. earn zero economic profits.

D. minimize cost per unit at their profit-maximizing quantity.

Answer: C

You might also like to view...

Why do we subtract import spending from total expenditures?

What will be an ideal response?

Which of the following best illustrates perfect competition?

a. Wheat farming. b. Orange growers setting quotas under the Sunkist cooperative. c. General Motors advertising campaign for its cars. d. All of these.

After the transaction in Table 13-1 is completed, what happens to actual reserves, required reserves, and excess reserves? Assume the required reserve ratio is 25 percent

a. Actual reserves increase by $10 million, required reserves increase $2.5 million, and excess reserves increase by $7.5 million. b. Actual reserves decrease by $10 million, required reserves decrease $2.5 million, and excess reserves decrease by $7.5 million. c. Actual reserves increase by $10 million, required reserves are unchanged, and excess reserves increase by $10 million. d. Actual reserves decrease by $10 million, required reserves decrease by $10 million, and excess reserves are unchanged.

A change in the price of a good causes: a. a change in the quantity demanded and therefore results in a movement along the given demand curve for the good. b. a change in demand and therefore results in a movement along the given demand curve for the good

c. a change in the quantity demanded and therefore results in a shift in the demand curve for the good. d. a change in demand and therefore results in a shift in the given demand curve for the good.