According to the neoclassical growth model, economic growth in the steady state occurs because of

a. increasing populations, which increase the demand for consumption.

b. exogenous increases in technology.

c. international trade.

d. active governments, which stimulate consumption through government spending.

e. all of the above.

B

You might also like to view...

Total output and total income in the circular flow model

A) are measures of the economy's level of savings. B) include only intermediate goods. C) are equal to each other. D) are related because national income is less than national product.

Economists believe that individuals:

A. have varying tastes for taking on financial risks, but are risk-averse in general. B. have the same tastes for taking on financial risks, and are risk-seekers in general. C. have varying tastes for taking on financial risks, but are risk-seekers in general. D. have the same tastes for taking on financial risks, and are risk-averse in general.

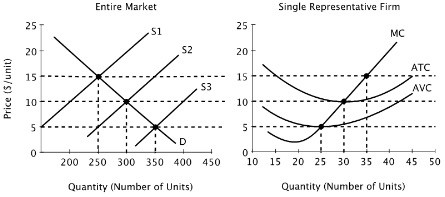

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive. The firm depicted in the graph on the right faces a demand curve that is:

The firm depicted in the graph on the right faces a demand curve that is:

A. the same as the marginal cost curve. B. the same as the market demand curve. C. horizontal at the market price. D. less than the market demand curve.

How do you calculate a percentage change in quantity if given an elasticity of demand and a percentage change in price?

What will be an ideal response?