What assumptions are necessary for a market to be perfectly competitive? Explain why each of these assumptions is important

What will be an ideal response?

The assumptions necessary for a market to be perfectly competitive are:

1. There are many buyers and sellers, all of whom are small relative to the market. This assumption ensures that each seller (or firm) and buyer is a price taker. A price taker cannot affect the market price.

2. All firms sell identical products. This condition excludes the possibility of any product differences which might justify different prices. Because the consumer cannot differentiate between products of different producers, any firm that charges a higher price will lose all its customers.

3. No barriers to new firms entering the market or exiting the market. This assumption guarantees that economic profits earned in the short run will be eliminated in the long run. In the long run, perfectly competitive firms will break even.

You might also like to view...

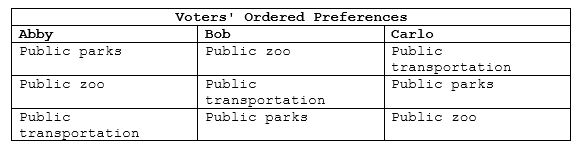

If a pair-wise majority vote was held and the voters' preferences are shown in the table, assuming public parks and the zoo was the first pair to be voted on, which option would win overall?

A. Public transportation

B. Public zoo

C. Public parks

D. Both Public parks and zoo.

In a closed economy private saving is $500 billion and the government budget deficit is $100 billion. What is investment?

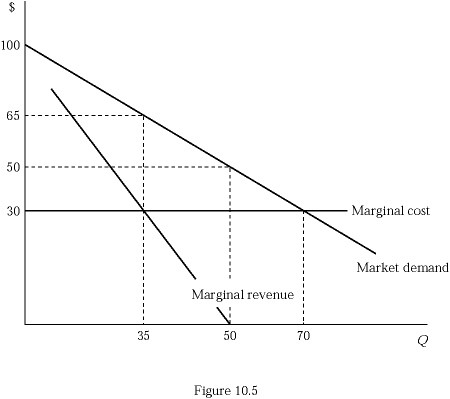

Suppose that Figure 10.5 shows an industry's market demand, its marginal revenue, and the production costs of a representative firm. If the industry was perfectly competitive, the consumer surplus would be:

Suppose that Figure 10.5 shows an industry's market demand, its marginal revenue, and the production costs of a representative firm. If the industry was perfectly competitive, the consumer surplus would be:

A. $2,450. B. $1,225. C. $612.50. D. $262.50.

If marginal utility is zero, total utility is

A. at its maximum. B. falling. C. zero. D. negative.