Suppose a perfectly competitive industry is in long-run equilibrium. If a decrease in demand leads to a lower long-run price, we know that

A) this is a decreasing-cost industry.

B) this is an increasing-cost industry.

C) some firms will be losing money in the long run.

D) after further adjustments, price will rise to its original level.

B

You might also like to view...

Hyperinflation refers to an inflation rate which exceeds 5 percent per month

Indicate whether the statement is true or false

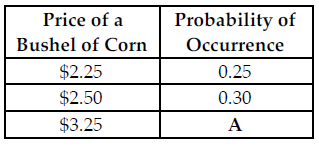

Refer to the table below. If these are the only three price options for a bushel of corn, what is the value of A?

The above table provides the possible prices for a bushel of corn next year along with the associated probabilities (in percent).

A) 0.55

B) 0.45

C) 0.25

D) 0.30

Productive efficiency means that goods and services are being produced by society in the least costly way.

Answer the following statement true (T) or false (F)

A society's production possibility frontier is bowed out from the origin because some resources are better suited for producing one good as opposed to the other.

Answer the following statement true (T) or false (F)