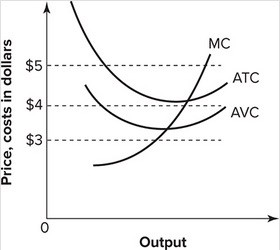

Refer to the graph shown. Suppose that the market price is $5. At this price, a perfectly competitive firm should:

A. continue to produce in the short run but shut down in the long run.

B. shut down immediately.

C. shut down in the short run but continue production in the long run.

D. continue to produce in both the short run and the long run.

Answer: D

You might also like to view...

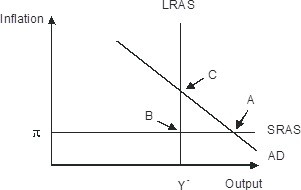

Refer to the figure below.________ inflation will eventually move the economy pictured in the diagram from short-run equilibrium at point ________ to long-run equilibrium at point ________,

A. Rising; B; C B. Falling; A; C C. Falling; A; B D. Rising; A; C

If the economy is in short run equilibrium then

A) real GDP equals potential GDP. B) nominal GDP equals potential GDP. C) real GDP cannot be equal to potential GDP. D) real GDP can be greater than, less than, or equal to potential GDP.

If a firm shuts down in the short run and produces no output, its total cost will be

a. zero b. equal to total variable cost c. equal to total fixed cost d. equal to explicit costs only e. impossible to calculate

An efficient allocation of resources requires each product's price to equal its marginal cost

a. True b. False Indicate whether the statement is true or false