Describe the relationship between marginal cost and average total cost

What will be an ideal response?

If marginal cost for a given output is below average total cost, average total cost will decrease as output increases but if marginal cost is above average total cost, average total cost will increase as output increases. If marginal cost equals average total cost, average total cost is at its minimum value.

You might also like to view...

The federal government can fund financially strained programs by

(a) Decreasing taxes (b) Increasing funding across all programs (c) Destroying money (d) Issuing U.S. Treasury bonds

A monopsony is a market in which

a. one firm is the sole producer of a good or service. b. one firm is the sole buyer of a good or service. c. firms encourage competition by starting "price wars" among competitors. d. firms collude in setting prices and levels of output.

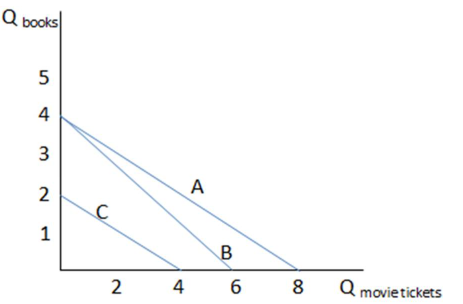

Assume Bryce's budget constraint is represented by line B in the graph shown. Which of the following would cause Bryce's budget constraint to shift to A?

A. The price of books increased.

B. The price of books decreased.

C. The price of movie tickets increased.

D. The price of movie tickets decreased.

An individual firm hiring labor in a competitive labor market faces a(n)

a. horizontal supply curve of labor b. backward-bending supply curve of labor c. downward-sloping supply curve of labor d. upward-sloping supply curve of labor e. vertical supply curve of labor