Explain what happens to the long-run supply curve of an industry when firm entry raises the price of inputs used in the industry

What will be an ideal response?

When firm entry raises the price of inputs used in the industry, the average total cost curve and marginal cost curves shift upward. This in turn causes the firms' short-run supply curves to shift upward when there is an increase in market demand. As a result, the long-run industry supply curve slopes upward.

You might also like to view...

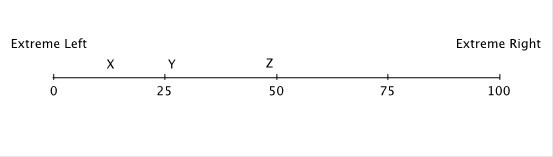

Hotelling's model has been used to describe differentiation in the political "market." Suppose that 100 voters are evenly distributed between the extreme left and the extreme right on the political spectrum, and that all voters vote, and they always vote for the candidate closest to them on this spectrum. The numbers on this spectrum represent the number of voters lying to the left of the number. So, at the midpoint, fifty voters lie to the left and fifty to the right. At the extreme right end, all 100 voters lie to the left. ![]()

width="553" />If Candidate Y is running against Candidate Z: A. Neither candidate has any incentive to move. B. Both candidates will have an incentive to move to the left. C. Candidate Y will have an incentive to move to the left, and Candidate Z will have an incentive to move to the right. D. Both candidates will have an incentive to move toward each other's position.

In a perfectly competitive market, the equilibrium price

a. is determined by all the buyers in the market but no single buyer is able to influence it b. is determined by all the sellers in the market but no single seller is able to influence it c. adjusts until the quantity supplied by all sellers is equal to the quantity demanded by all buyers d. is not influenced by the cost structure of the firms in the market e. is not influenced by the preferences of the consumers in the market

The expansion path of product indifference curves shows the cost-minimizing combination of inputs

a. True b. False Indicate whether the statement is true or false

When new firms enter a perfectly competitive market,

a. demand increases. b. the short-run market supply curve shifts right. c. the short-run market supply curve shifts left. d. existing firms will increase prices to keep the new firms from entering.