The only two firms in a market are trying to decide what price to charge. The payoff matrix for this duopoly game is shown above. The payoffs are thousands of dollars of economic profit. Which of the following statements is correct?

A) If the firms play this game repeatedly, one would end up charging $20 and the other $10.

B) If the firms cooperate, they could both earn $55,000 in economic profit.

C) The Nash equilibrium in this game is for both firms to set P = $20 because that maximizes their combined profit.

D) Firm B's strategy is to always set P= $20 because that gives Firm B the highest possible profit.

E) If Firm B sets P = $20, then Firm A will maximize its profit by setting its P = $20.

B

You might also like to view...

If the Fed is worried about inflation and wants to raise the interest rate, in the short run it can

A) increase the demand for money. B) decrease the demand for money. C) increase the quantity of money. D) decrease the quantity of money. E) directly raise the interest rate without affecting either the demand for money or the supply of money.

List and explain the factors that can increase labor productivity

What will be an ideal response?

Economists typically define money as:

A. anything in which its value can be inflated. B. a means of payment that lacks intrinsic value. C. currency that is issued by a central bank. D. a widely accepted means of payment.

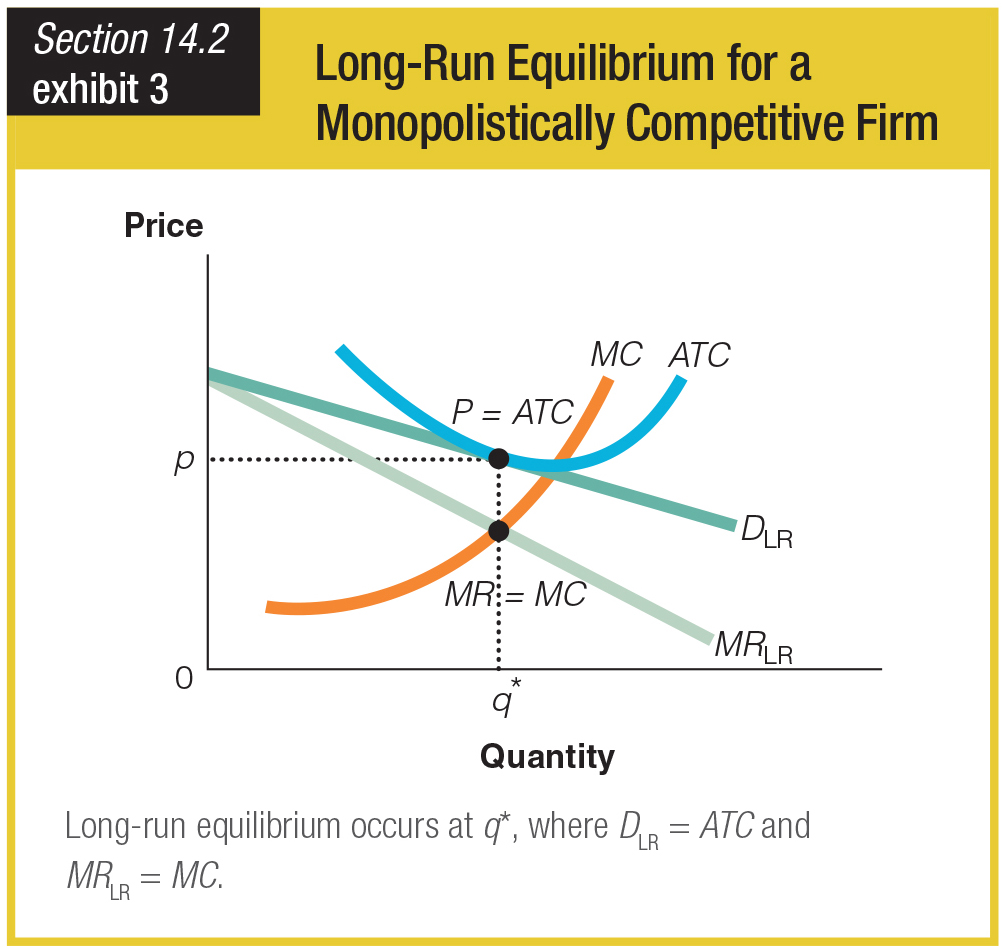

Which of the following accurately describe where long-run equilibrium happens in the monopolistically competitive firm?

a. At P and q*, long-run demand equals average marginal cost and long-run marginal revenue equals total cost.

b. At 0 and q*, long-run demand equals average total cost and long-run marginal revenue equals marginal cost.

c. At P and q*, long-run demand equals average total cost and long-run marginal revenue equals marginal cost.

d. At 0 and q*, long-run demand equals average marginal cost and long-run marginal revenue equals total cost.