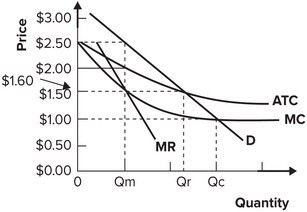

Refer to the graph shown. If the price of the product is $1 and the firm is a natural monopoly:

A. there will be a surplus of the product.

B. the firm can earn profit by producing more than Qc.

C. the firm will incur losses by producing the quantity demanded at that price.

D. the firm will earn economic profit by satisfying the market quantity demanded at that price.

Answer: C

You might also like to view...

Over time, the percentage of total employment in services has ________ and in agriculture, employment has ________

A) increased; increased B) decreased; increased C) stayed about the same; decreased D) stayed about the same; increased E) increased; decreased

External benefits are those that accrue:

A. directly to the decision maker of a market exchange. B. indirectly to the decision maker of a market exchange. C. without compensation to someone other than the person who caused it. D. to the government without its direct intervention.

An oligopolistic market may be difficult to enter because of government regulation or the expense of nonprice competition.

Answer the following statement true (T) or false (F)

Which of the following questions is not answered by general equilibrium analysis?

A. What outcome is most desirable for the whole society? B. How will a change in one market affect another market? C. Can all markets simultaneously be in equilibrium? D. Are equilibria in different markets compatible with one another?