If a firm has determined its optimal output level, where MR = MC, then price

A. is unchanged.

B. is set by statistical analysis of the market.

C. is equal to MC.

D. is determined by the market demand at that output.

Answer: D

You might also like to view...

Starting from long-run equilibrium, a large decrease in government purchases will result in a(n) ________ gap in the short-run and ________ inflation and ________ output in the long-run.

A. expansionary; lower; potential B. expansionary; higher; potential C. recessionary; lower; potential D. recessionary; lower; lower

An international producer is trying to centralize its R&D. This is consistent with it trying to

a. Set up a functional division b. Take advantage of the economies of scale c. Take advantage of the learning curve effect d. All of the above

Which of the following statements is TRUE about the price that a monopolist charges?

A. The difference between the price charged by a monopolist and a perfect competitor is due to differences in costs. B. Too much of the good is being produced in a competitive market and not enough is being produced in a monopoly. Due to the way that prices are set. C. The price is the same as the price that would be charged if there was perfect competition. D. The value that society places on the last unit produced in a monopoly is greater than its cost.

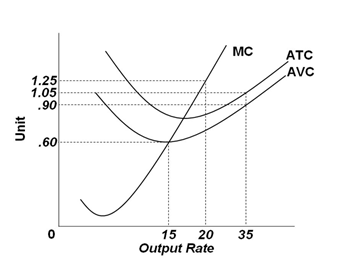

Refer to the graph below. It shows the cost curves for a competitive firm. What is the lowest price at which the firm will start producing output in the short run?

A. $1.25

B. $1.05

C. $0.90

D. $0.60