In the market for cotton, suppose the equilibrium price is $10 per ton and the equilibrium quantity is 100 tons. If the government then imposes a price support of $20 per ton,

A) marginal benefit exceeds marginal cost.

B) the market becomes more efficient

C) marginal cost decreases.

D) the government must supply some cotton to offset the shortage that results.

E) marginal cost exceeds marginal benefit.

E

You might also like to view...

Answer the following statement(s) true (T) or false (F)

1. Incremental costs are the accumulated expenditures associated with an environmental policy initiative. 2. When implementing environmental policy, all expenses paid by the government plus compliance costs paid by all economic sectors are known as explicit costs. 3. Fixed costs are controllable in the short run but not the long run. 4. The accounting equivalent of variable costs is capital costs. 5. The value of reduced product variety due to an environmental policy initiative or regulation is an example of an implicit cost.

How does an increase in the price of laptop memory chips affect the market of laptops?

a. The demand curve for laptops shifts to the right b. The demand curve for laptops shifts to the left c. The supply curve for laptops shifts to the right d. The supply curve for laptops shifts to the left

The total consumer surplus enjoyed by all consumers in a market

a. exceeds the market price b. is measured by the area under the market demand curve c. is measured by the area beneath the market price d. is a Pareto improvement e. is called market consumer surplus

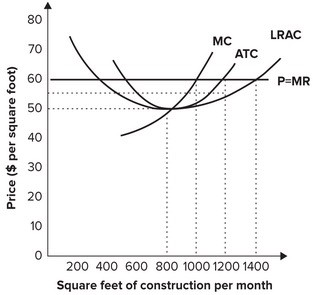

Refer to the graph shown. Assuming that the industry operates under conditions of perfect competition and that the firms seek to maximize profits, this firm will:

A. produce 1,200 square feet of construction in the short run. B. incur economic losses in the short run. C. produce 800 square feet of construction per month in the short run. D. produce 1,000 square feet of construction per month in the short run.