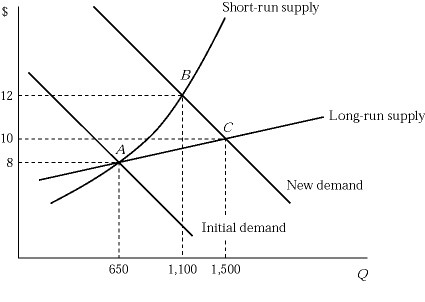

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the short run?

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the short run?

A. The market price rises to $12, which is greater than the average total cost.

B. Each existing firm maximizes its profit by producing the output where marginal cost equals $12.

C. Each existing firm produces two more units per hour, compared to its initial profit-maximizing output level at point A.

D. All of these are correct.

Answer: D

You might also like to view...

Producer surplus is

a. measured using the demand curve for a good. b. always a negative number for sellers in a competitive market. c. the amount a seller is paid minus the cost of production. d. the opportunity cost of production minus the cost of producing goods that go unsold.

Value added is calculated by:

A. subtracting the cost of materials used in production from the value of sales. B. adding the cost of materials used in production to the value of sales. C. adding the value of output to the value of inputs. D. subtracting the value of sales from the cost of materials used in production.

Which of the following is closest to a perfectly competitive market?

A. the market for breakfast cereal B. the market for automobiles C. the market for corn D. the pizza market

In developed countries, the enforcement of contracts and the adjudication of contract disputes through the court system:

A. reduces the volume of international trade. B. is an important way to reduce transaction costs. C. lowers the comparative advantage enjoyed by producers. D. weakens the system of property rights.