Scarcity is best defined as

a. unlimited resources

b. a shortage -- when buyers cannot obtain the goods they want

c. a surplus -- when sellers cannot sell the goods they produce

d. insufficient resources to satisfy unlimited wants

e. the private ownership of society's resources

D

You might also like to view...

Is it theoretically possible for general equilibrium to be attained? Is it likely that general equilibrium will be attained? Explain

What will be an ideal response?

Why did the United States suspend its preferential trade treatment for Bangladesh in 2013?

a. The United States wanted to collect more tariff revenue on all imports from Bangladesh. b. The United States wanted to punish Bangladesh for its poor labor practices. c. The United States wanted to collect more tariff revenue on imports other than garments from Bangladesh d. The United States wanted to force Bangladesh to join NAFTA.

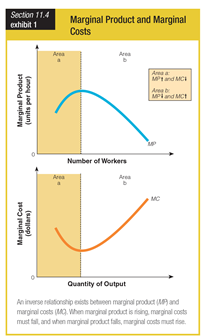

Initially, when workers are added, marginal product rises and marginal cost falls. Why is this the case?

a. Total product increases by a fixed amount with each additional employee.

b. The equipment is new, and no repair or maintenance costs have set in yet.

c. Marginal costs are fixed costs that are spread over a larger number of employees.

d. Each additional worker is adding more to the total output than the previous worker.

Explain why national income and domestic product must be equal.

What will be an ideal response?