In the long run, perfect competition results in firms producing

a. at the minimum point of their long-run average cost curves, which indicates allocative efficiency.

b. where price equals marginal cost, which indicates economic efficiency.

c. where price equals marginal cost, which indicates the optimal scale of operation.

d. at the minimum point of their long-run average cost curves, which indicates economic efficiency.

d. at the minimum point of their long-run average cost curves, which indicates economic efficiency.

You might also like to view...

Explain how the volunteer's dilemma is a special case of the public goods problem in which the possibility exists that no one will end up providing the public good

What will be an ideal response?

For quantity exchanged to decrease, but the price to rise, there must have been a(n)

a. increase in demand. b. decrease in demand. c. increase in supply d. decrease in supply.

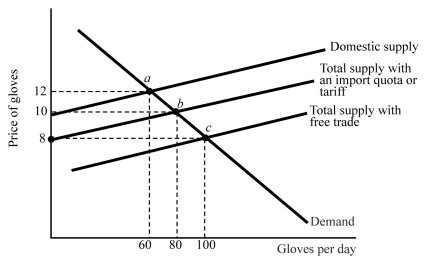

Refer to Figure 18.1. With free trade, what is the equilibrium quantity of gloves in Duckland?

Refer to Figure 18.1. With free trade, what is the equilibrium quantity of gloves in Duckland?

A. 100 B. 80 C. 60 D. 40

On the long-run aggregate supply curve

A) a decrease in the price level decreases the level of potential GDP. B) a decrease in the price level increases the aggregate quantity of GDP supplied. C) a decrease in the price level decreases the aggregate quantity of GDP supplied. D) a decrease in the price level has no effect on the aggregate quantity of GDP supplied.