A country's production possibilities boundary shows that

A) when a society combines its resources inefficiently, it cannot produce more of one good without

producing less of the other good.

B) the supply for goods always exceeds the demand.

C) all points inside the boundary are preferred to all points on the boundary.

D) when a society combines its resources efficiently, it is always possible to produce more of all goods.

E) when a society combines its resources efficiently, it cannot produce more of one good without producing

less of the other good.

Answer: D) when a society combines its resources efficiently, it is always possible to produce more of all goods.

You might also like to view...

Suppose the market demand for milk is Qd = 150 - 5P. Additionally, suppose that a dairy's variable costs are VC = 2Q2 (where Q is the number of gallons of milk produced each day), its marginal cost is MC = 4Q and there is an avoidable fixed cost of $50 per day. In the long run there is free entry into the market. Suppose the demand for milk doubles. What is the new long-run equilibrium quantity?

A. 50 B. 60 C. 100 D. 120

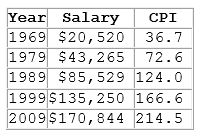

If the 1989 salary in 2009 dollars is $147,951, how do we interpret this?

A. The salary earned in 1989 could have purchased the same amount of goods as $147,951 could buy in 2009.

B. It would take $147,951 in 2009 to buy the same amount of goods that was purchased in 1989 with $85,529.

C. Someone earning $85,529 in 1989 would be as well off if he were earning $147,951 in 2009.

D. All of these interpretations are correct.

If the government does not react to a recession:

A. the economy will remain out of its long-run equilibrium indefinitely. B. the economy will recover, but much more slowly. C. voters and consumers are likely to be happy with less government interference. D. the government generally doesn’t engage in any policy during a recession.

If the income elasticity of demand is negative, this means that the good is

a. an inferior good b. sold at a lower than equilibrium price c. provided by a monopoly producer d. provided by competitive producers e. a normal good