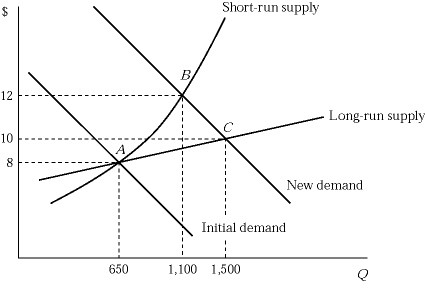

Figure 9.5Figure 9.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the short run?

Figure 9.5Figure 9.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the short run?

A. The market price rises to $12, which is greater than the average total cost.

B. Each existing firm maximizes its profit by producing the output where marginal cost equals $12.

C. Each existing firm produces two more units per hour, compared to its initial profit maximizing output level at point A.

D. All of these are correct.

Answer: D

You might also like to view...

If the United States can increase its production of automobiles without decreasing its production of any other good, the United States must have been producing at a point

A) within its PPF. B) on its PPF. C) beyond its PPF. D) None of the above is correct because increasing the production of one good without decreasing the production of another good is impossible.

Refer to Table 20-1. The unemployment rate for this simple economy equals

A) (100/1,000 ) × 100. B) (100/15,000 ) × 100. C) (100/1,100 ) × 100. D) (100/20,000 ) × 100.

A firm using a two-part tariff faces a tradeoff because

A) any increase in consumer surplus must be offset by a decrease in producer surplus. B) the only way to increase the fixed-fee portion of the price is to lower the per-unit portion of the price. C) the only way to increase total revenue is to lower per-unit profit. D) the smaller the variation between the parts of the price, the greater the deadweight loss generated by the pricing scheme.

A market with few sellers, some influence over price, high barriers to entry, a differentiated product, and non-price competition is known as

A) perfect competition. B) monopolistic competition. C) oligopoly. D) monopoly.