If price rises, what happens to the quantity demanded for a product?

a. It does not change.

b. It decreases.

c. Uncertain--economic theory has no answer to this question.

d. It increases.

b. It decreases.

You might also like to view...

Consider the following:

(i) Suppose the government imposes new regulations that force tire manufacturers to incur some one-time expenses for factory safety improvements. Will the new regulations raise the price of tires? Why or why not? (ii) Suppose the government imposes new regulations that force tire manufacturers to adopt cleaner production methods that raise the production cost by $10 per tire. Will the new regulations raise the price of tires? Why or why not?

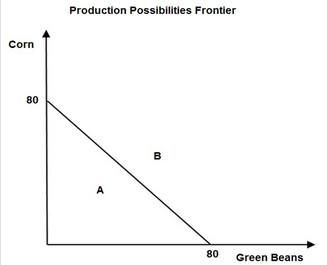

Use the following figure to answer the question below. A point on the production possibilities frontier in the figure above is

A point on the production possibilities frontier in the figure above is

A. not attainable. B. inefficient. C. local. D. efficient.

Explain the concept of an accounting identity

What will be an ideal response?

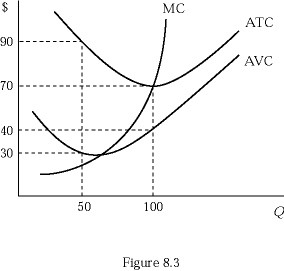

Figure 8.3 shows a firm's marginal cost, average total cost, and average variable cost curves. The firm's total fixed cost is:

Figure 8.3 shows a firm's marginal cost, average total cost, and average variable cost curves. The firm's total fixed cost is:

A. $2,800. B. $3,000. C. $4,500. D. $7,000.