In a perfectly competitive market, the price of the product is

a. independently set by each competing firm

b. set by the market leader and then copied by other firms

c. jointly set after a meeting of all firms in the market

d. set by market supply and demand

d. set by market supply and demand

You might also like to view...

The budget line and the indifference curve are geometric devices used to provide a closer look at consumer choice.

Answer the following statement true (T) or false (F)

The most likely substitute good for hot dogs would be:

A. ketchup. B. burgers. C. potato chips. D. a plate.

Due to the huge number of consumers, the market demand curve for chocolate is ______.

a. intermittent

b. stepped

c. smooth

d. zig-zagged

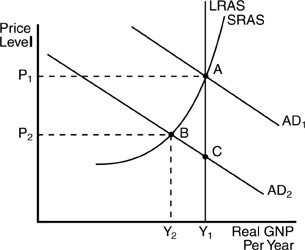

Suppose the economy is initially operating at point A in the above figure. Which of the following statements is TRUE?

Suppose the economy is initially operating at point A in the above figure. Which of the following statements is TRUE?

A. An unexpected reduction in aggregate demand will cause the economy to move from point A to point C in the short run. B. An unexpected reduction in aggregate demand will cause the economy to move from point A to point B in the long run. C. An unexpected reduction in aggregate demand will cause the economy to move from point A to point B in the short run. D. none of these