Explain the meaning of the “marginal rate of substitution.”

Please provide the best answer for the statement.

An indifference curve shows all the combinations of two products, X and Y that will give the consumer the same level of satisfaction or utility. Indifference curves are down sloping because of the inverse relationship between products X and Y. To obtain more of product X means giving up some total utility from product Y. Indifference curves are also convex to the origin. Thus, the slope of an indifference curve diminishes as you move down the curve. The reason for the diminishing slope is that the marginal rate of substitution of product X and Y falls as you move down the curve. As the consumer moves down the indifference curve, the consumer is willing to give up less of Y to get more of X. The marginal rate of substitution is the slope of the indifference curve at any point.

You might also like to view...

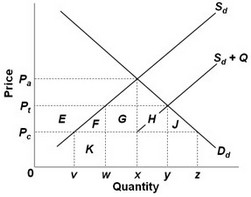

Use the following graph, where Sd and Dd are the domestic supply and demand for a product and Pc is the world price of that product, to answer the next question. Sd + Q is the product supply curve after an import quota is imposed. A quota of y?w will result in an increase of domestic producer surplus equal to area(s)

Sd + Q is the product supply curve after an import quota is imposed. A quota of y?w will result in an increase of domestic producer surplus equal to area(s)

A. E + F + K. B. E. C. E + F + G + H + J. D. K.

What are the effects of a financial crisis on short-run aggregate supply? How might long-run aggregate supply be affected?

What will be an ideal response?

If society leaves some of its resources unemployed, then it will be operating at a point:

a. beneath its production possibilities curve. b. at a corner of its production possibilities curve. c. anywhere along its production possibilities curve. d. outside of its production possibilities curve.

It may seem paradoxical but according to ___________ when tax rates increase—at least beyond a certain rate—tax revenues fall and when tax rates fall, tax revenues increases

a. Professor Phillips and other neo-Keynesian economists b. Professor Laffer and other supply-side economists c. Professor Ricardo and other classical economists d. Professor Barro and other rational expectations economists e. Professor Samuelson and other Keynesian economists