When positive economic profits exist in an industry:

A) the market price of the good produced by the industry is less than the average total cost of the industry.

B) resources flow from less productive uses to that particular industry.

C) there is an exit of firms from the industry.

D) the market price of the good produced by the industry is less than the marginal cost faced by the industry.

B

You might also like to view...

Between 1981 and 2013, the overall mortality rate in the United States

A) remained fairly constant. B) decreased by more than 25 percent. C) slowly but steadily increased. D) was similar to the average rate in most low-income countries.

Explain how long-run economic profits are linked to entry in monopolistic competition and perfect competition

What will be an ideal response?

If the marginal product of labor rises, the marginal cost of output

a. rises b. falls c. remains constant d. rises and then falls e. dampens

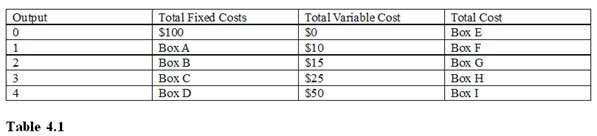

Referring to Table 4.1, Box F should be filled with

A. $0. B. $100. C. $10. D. $110.