Which type of compensation method works by performance bonus?

A. Profit sharing

B. Piece rate

C. Revenue sharing

D. All of the statements associated with this question are correct.

Answer: D

You might also like to view...

The potential problem with competitive pricing regulation of a natural monopoly is that ________.

A. P < MR B. P < ATC C. P < AVC D. P < MC

Joe's Imports is currently the only dealer for imported Sporto autos on the East Coast, but Fred's Autos may enter the import market and start selling Sporto cars in the East Coast market during the coming year

Joe's Imports can pay the Sporto manufacturer for exclusive East Coast marketing rights, which would deter the entry of Fred's Autos into the market. The payoffs from the possible actions are measured in millions of dollars per year, and the possible outcomes of the sequential entry game are summarized in the following matrix: Fred's Autos enters Fred's Autos does not enter Joe's Imports buys rights ---- 50, 0 Joe's Imports does not buy 40, 40 80, 0 What is the equilibrium outcome from this sequential entry game? A) Joe's Imports buys the marketing rights, and Fred's Autos cannot enter the market. B) Joe's Imports buys the marketing rights, and Fred's Autos enters the market. C) Joe's Imports does not buy the marketing rights, and Fred's Autos enters the market. D) Joe's Imports does not buy the marketing rights, but Fred's Autos does not enter the market.

Answer the following questions true (T) or false (F)

1. Consumer surplus is the difference between the highest price someone is willing to pay for a product and the price he actually pays for the product. 2. Producer surplus is the difference between the lowest price a firm is willing to accept for a product and the price it actually receives for the product. 3. The total amount of consumer surplus in a market is equal to the area below the demand curve.

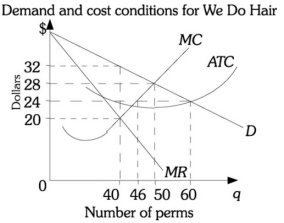

Refer to the information provided in Figure 15.2 below to answer the question(s) that follow.  Figure 15.2 Refer to Figure 15.2. In this monopolistically competitive industry, in the long run

Figure 15.2 Refer to Figure 15.2. In this monopolistically competitive industry, in the long run

A. demand for the product will decrease so that profits are decreased. B. the government will impose price controls to eliminate any economic profits. C. firms will continue to earn economic profits. D. firms will enter until all firms earn a normal profit.