Perfect competition and pure monopoly are concepts useful primarily for realistic applications.

Answer the following statement true (T) or false (F)

False

You might also like to view...

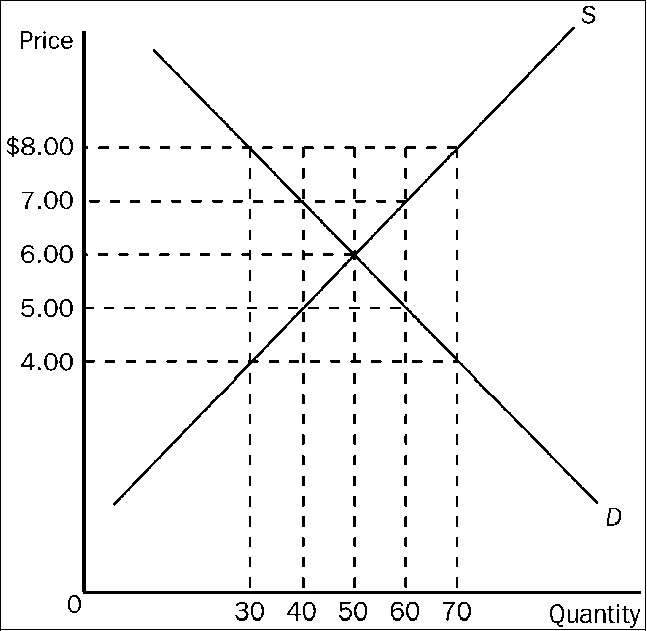

Figure 4-17

Refer to . Suppose a price ceiling of $4.50 is imposed. As a result,

a.

there is a shortage of 15 units of the good.

b.

the demand curve will shift to the left so as to now pass through the point (Q = 35, P = $4.50).

c.

the situation is very much like the one created by a binding minimum wage.

d.

the quantity of the good that is bought and sold is the same as it would have been had a price floor of $7.50 been imposed.

A risk-loving individual would:

A. prefer a risky prospect with an expected value of $5 to a certain amount of $5. B. prefer $5 with certainty to a risky prospect with the expected value of $5. C. be indifferent between a risky prospect with an expect value of $5 and a certain amount of $5. D. prefer a risky prospect with the expected value of $0.50 to $5 with certainty.

The following statements about the "sunk cost fallacy" are true, except:

A. It's the tendency to drag past costs into current marginal cost-benefit calculations B. It comes from a desire to "get one's money's worth" out of a past expenditure C. It refers to the fact that average fixed costs are not a major part of production costs D. It could lead one to "throw good money after bad"

For a monopolist, price

A. can be greater than or less than marginal revenue. B. is greater than marginal revenue. C. is less than marginal revenue. D. equals marginal revenue at all output levels.