Under both perfect competition and monopoly, a firm:

A. is a price taker.

B. is a price maker.

C. will shut down in the short-run if price falls short of average total cost.

D. sets marginal cost equal to marginal revenue.

Answer: D

You might also like to view...

If the consumption of a good decreases the quantity available for another person, the good is rival

Indicate whether the statement is true or false

market with four firms in competition with each other has a equilibrium price of $25 and equilibrium quantity of 200,000. If the four firms form a cartel, the cartel, set price will be ________ than $25 and the set quantity will be ________ than 200,000.

A) greater; less B) less; greater C) greater; greater D) less; less

Which of the following statements about markets is true?

a. Markets reduce the opportunity costs of making exchanges. b. Markets expand the range of buyers and sellers available as counterparties. c. Markets increase the transaction costs of making exchanges. d. Markets increase the costs of information.

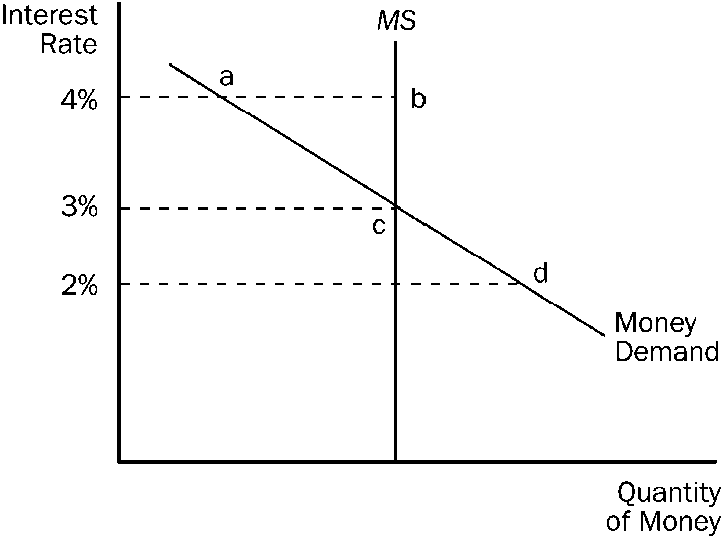

Figure 14-8

Refer to . At an interest rate of 4 percent there is excess

a.

money demand equal to the distance between a and b.

b.

money demand equal to the distance between b and c.

c.

money supply equal to the distance between b and a.

d.

money supply equal to the distance between c and b.